Who Controls the On-Ramp to Generative AI?

What OpenAI’s missed targets and Alphabet’s blowout quarter tell us, and don’t tell us, about who controls the on-ramp to generative AI

By Osbaldo Franco, Founder & Principal, Mod7 Research Strategy

April 30, 2026

Yesterday was one of those rare days when two competing narratives about the same market land almost simultaneously. While markets were still digesting The Wall Street Journal’s report that OpenAI has missed several self-imposed user growth and revenue targets since late 2025, Alphabet posted a blockbuster first quarter that validated the current Gemini strategy in almost every conceivable metric.

The juxtaposition of the two news stories is hard to ignore. For anyone tracking the competitive dynamics of the generative AI assistant market, it raises a pair of questions worth considering: Are we witnessing the start of a change of the baton? Or just a short-lived stumble by the incumbent who is still winning the race by every measure?

First, the news as it stands

On one side, OpenAI has missed a string of internal benchmarks, including the goal of one billion weekly active ChatGPT users by the end of 2025 and multiple monthly revenue targets in early 2026. Competitive pressure from Anthropic in coding and enterprise, and Gemini pressing on the consumer side, are contributing factors at a moment when the company is preparing for a potential IPO.

On the other side, Alphabet’s Q1 2026 results read like the counter-argument. Gemini Enterprise paid monthly active users grew 40% quarter-over-quarter. API usage surpassed 16 billion tokens per minute, up 60% from the prior quarter. Google Cloud crossed $20 billion in quarterly revenue for the first time, growing 63% year-over-year. Search traffic hit record highs, driving 19% revenue growth despite earlier fears of revenue cannibalization with its AI integration. Alphabet CEO, Sundar Pichai, called it the strongest quarter ever for consumer AI plans. Two companies, two trajectories, same week.

What Our Research Says About the Gateway Dynamic

The Mod7 Beyond AI Adoption report documented a pattern we called the Gateway Hypothesis, and this week’s news gives it immediate relevance.

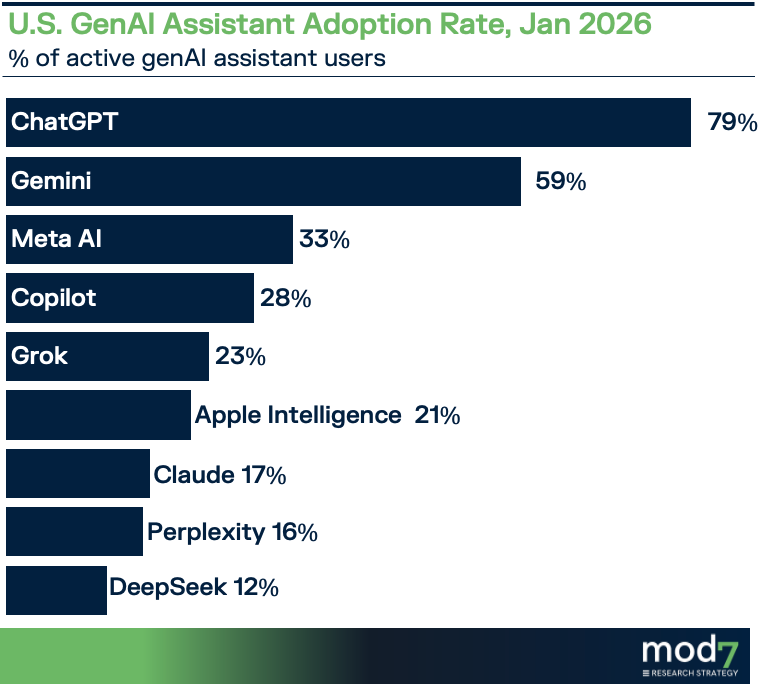

Our data showed that ChatGPT functions as the universal on-ramp into the generative AI assistant category. Its adoption rate of 79% among genAI users is unmatched. Correlation analysis revealed that ChatGPT is the only platform with a statistically significant negative relationship between usage frequency and share of time. That means that as users build broader AI toolkits, ChatGPT's share of their attention decreases, but its adoption holds. The signature of a gateway: a tool users enter through, not one they exit entirely. Its replacement risk (13%) is the lowest in the study.

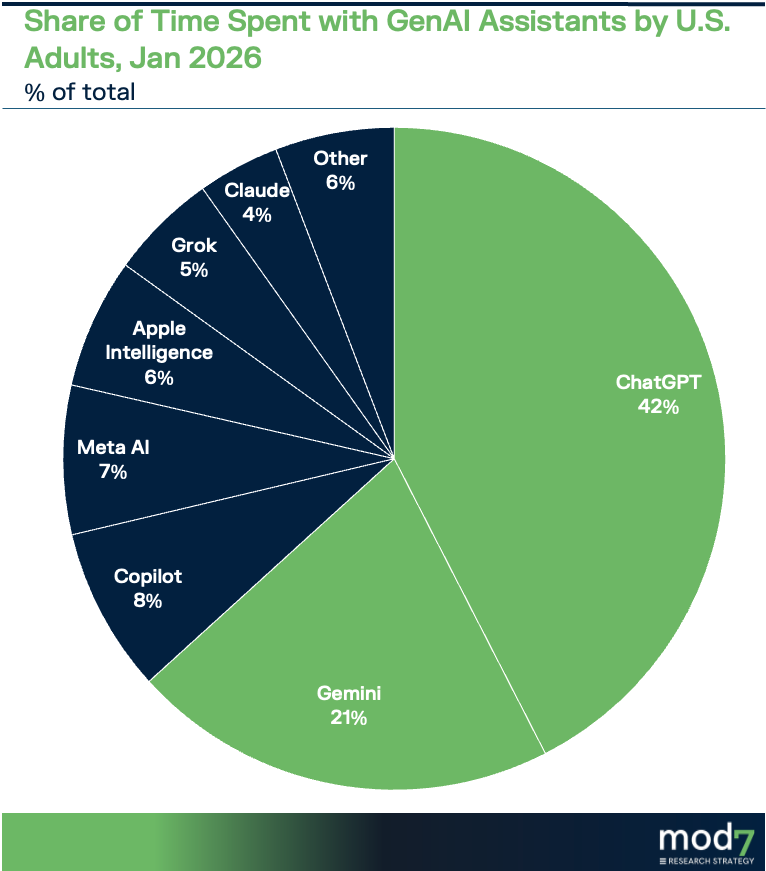

Gemini, in January 2026, was the most significant challenger by volume with a 59% adoption and a 21% share of time spent. More importantly, it led the market in net forward intent by a wide margin: +20 percentage points, compared to ChatGPT's +11 and single-digit scores for every other platform.

That number mattered then. It looks even more important now.

Gemini’s momentum is real, but so are its limitations

Alphabet's Q1 2026 results confirm that the Gemini momentum measured in our January survey was not a blip. Enterprise adoption is accelerating. Developer usage is surging. Consumer subscriptions are growing. The integration across Search, Workspace, Maps, and YouTube gives Gemini a distribution flywheel that no standalone AI assistant can replicate.

But the Mod7 data also surfaced a structural gap. Gemini users remain clustered in curiosity and experimentation tasks (Index 106) and knowledge support (100). Basically, an enhanced search experience. Gemini users under use the Alphabet assistant in creative tasks (Index 89), health and wellness (86), and analytics (75). These are not marginal categories. They are precisely the high-frequency, high-engagement activities that define the heaviest AI users, the daily omnivores who leverage their AI toolkit with the most distinct activities, 15.4 on average.

The on-ramp role has historically belonged to the platform that covers the most ground for the most users, not the one that deepens a handful of use cases. ChatGPT's engagement indices hover between 97 and 110 across all 13 activity families we measured, a genuine Swiss Army knife profile. Gemini's user base, at least in January, was still behaving more like it had adopted a smarter, faster version of Google Search than a new cognitive platform.

The gap is real, but the Q1 2026 earnings suggest Gemini is now positioned to close it.

Is the baton being passed?

My honest read of all of this: not yet, but the conditions for a transition are building up.

OpenAI's stumble matters because the gateway function is the first experience that converts a skeptic into a habitual user. Our data showed that 39% of never-users said nothing would motivate them to try the technology. The potential converts are still out there, but they are not waiting for a faster model. They are waiting for a reason to trust the category.

Gemini's tailwind demonstrates the Google ecosystem is the closest thing the market has to an infrastructure advantage in consumer AI. A user who encounters Gemini through Search, Workspace, or through an Android device is encountering it in a context where trust already exists.

What about Claude?

Our data placed Claude at a 17% adoption rate, niche by market standards, but with a technical task engagement index of 167, meaning its users are 67% more likely than the average genAI user to engage it for high-fidelity professional work. Claude has a 44% replacement risk, however, reflecting the project-based nature of user engagement: cycle in, deliver, cycle out. Its share of time spent, however, grows as users expand their toolkits.

The competitive story here is not simply OpenAI versus Gemini. Watch for a three-way market structure: a generalist on-ramp, an ecosystem-integrated daily utility, and a high-trust specialist for professional work. The platform controlling habitual, high-frequency engagement will have the most leverage over the agentic commerce model the industry is actively building. That platform is not yet decided.

The baton is not changing hands today. But it is wobbling in ways that, as recently as six months ago, would have seemed unlikely. The race is getting interesting.